Lesson 14: Single or Double Entry Accounting

In the last lesson, we discussed accounting and why there is a benefit to not only keeping accurate records but how it can also drive your business forward.

It doesn’t mean you have to be a trained financial accountant, but knowing where your money is going and how you are getting it in is a big step to realising the potential your business has.

If you have missed any of the other modules of the course, have a look at How to Start a Market Stall and find out how you can be a better market stall trader.

Types of Accounts

Within the scope of this website and blog, I will only be discussing Single Entry Accounting and Double Entry Accounting. If you feel you are on the scope of Enron, then I think you may need to consult a qualified accountant and a very good lawyer!

The way we account for our money can be as simple as placing money in a tin and then taking money out of that tin. This is essentially what accounting look like.

There are very complex ways to account, and although I am aware of this form of witchcraft, I choose to only understand it and no more.

If we can continually think about that tin with the money in it, then accounting will become very easy to the market trader. Grasping this concept will empower the market trader to be better at budgeting and developing their products.

The Power of the Money Tin

Okay, so we have our imaginary tin (Some of you may have a real one and that’s fine too), and as with every business you need to put money in the ‘tin’ to get started. This is known as capital for the business.

Okay, so we have our imaginary tin (Some of you may have a real one and that’s fine too), and as with every business you need to put money in the ‘tin’ to get started. This is known as capital for the business.

Once the money is in the tin, you can now move forward and begin planning your stall and your products. Your new business may be to sell pancakes on a small market stall. This is what you will need to start trading:

- Stove/gas ring/fire

- Electricity/gas/wood

- Frying Pan

- Ladle

- Spatula

- Oil

- Eggs

- Flour

- Milk

- Sugar

- Lemon

- Cinnamon

- Syrup

- Serviettes

- Plates

- Hygiene licence

- Table Cloth

- Float box

- Small Change

- Cleaning items

- etc…

This is all for a simple stall and all these items are part of the startup cost. That must all come out of the “Tin” – out of the capital.

Now you may already have a gas stove, a frying pan and even the ladle and spatula, so if you are going to add those to your business, consider them as capital too, it is just that you have added actual items to the tin.

Now you need to buy the ingredients and will come from the start-up capital you placed in the tin. Your rent for the day must come from the start-up capital and any other items, like transport or storage costs.

See how big this tin is getting?

Whatever you use for your stall and buy for it, must first come from the ‘tin’ and also return to the ‘tin’. Think of the money as changing into physical items and then magically as you sell something it changes back into money again. Cool thought ha!

Keeping Records

You may have noticed that I very quickly had a lot of things going into the tin, then out of it again and then back into it. These are known as transactions and this is what needs to be recorded.

The way you put things into the tin and take them out is what accounting is. The more detailed you make it the more you can analyse your business results.

Think of it this way, if I can show in one month how much flour I bought and how much I still have left, I know how much I can budget for flour next month.

Then we can budget over the year too.

Same for your transport. If every time you go to a market you list how much fuel you use or how much the transport was to get there and back, you will have a better idea of how much your transport bill is costing you month by month.

That is all accounting is trying to do. Make sense of what you are spending on and where you are receiving it from. Our brains are fantastic at recording the information we like, but we don’t hold accurate records of things we don’t like. The brain filters that all out.

Your guess at how your business is going is just that… a guess, and that is not how you will be able to grow!

How to use Receipts

Most of the time you will receive a receipt, or be asked if you need one – TAKE IT!

This is a record for you that you need to put in the ‘tin’. Think of the money that was in the tin as changing into a receipt. When it comes to later on when you are checking where the money has gone or explaining how you changed it, you will have the receipt to guide you, with a time and day attached to it.

This is known as reconciling, and you are really just making sure you have a true record for your money.

KEEP EVERY SINGLE ONE! Even print off the ones you receive electronically.

I know, sounds silly doesn’t it? Okay, this is really down to how you feel most comfortable, but you essentially need to keep these receipts for 5 to 7 years.

Some countries now allow the scanning of receipts as records, but if you want to make sure everything is covered, keep them all in a box, correctly filed and stored away, in the loft or someplace safe.

The way that seems easiest to do this, is to collect your receipts in a shoebox for that day or for that week. (I recommend day as it makes your book-keeping so much easier.) When that day or week is finished, reconcile each to your accounting records and place them in a plastic wallet in date order.

Sure, by now you just think this as pedantic, but hold on.

Label the plastic with the day or week, and place it into a filing box. Then repeat as each week passes.

Once a month is done, you can ‘close’ that plastic wallet and start again for the next month. Keeping everything in order going from back to front!

When you get to the end of the year, you make sure everything is placed in one box (if possible), label it and then place it out the way and forget about it. You are done with it until you or someone else needs to check something and you will find it easy to do that later on.

Right, enough about organisation and onto the accounting side…

Single Entry Accounting

If you are a small stall owner, you are probably using this method or will at least start with the method as it is the simplest way to keep your accounts.

You are normally a one-person enterprise, and you do not need to worry about shares in the company and paying other employees or shareholders.

It is as it sounds too, you write down on one line:

- When you paid or received something (Service or product)

- What it was (Brief description)

- Amount

- Keep a running total

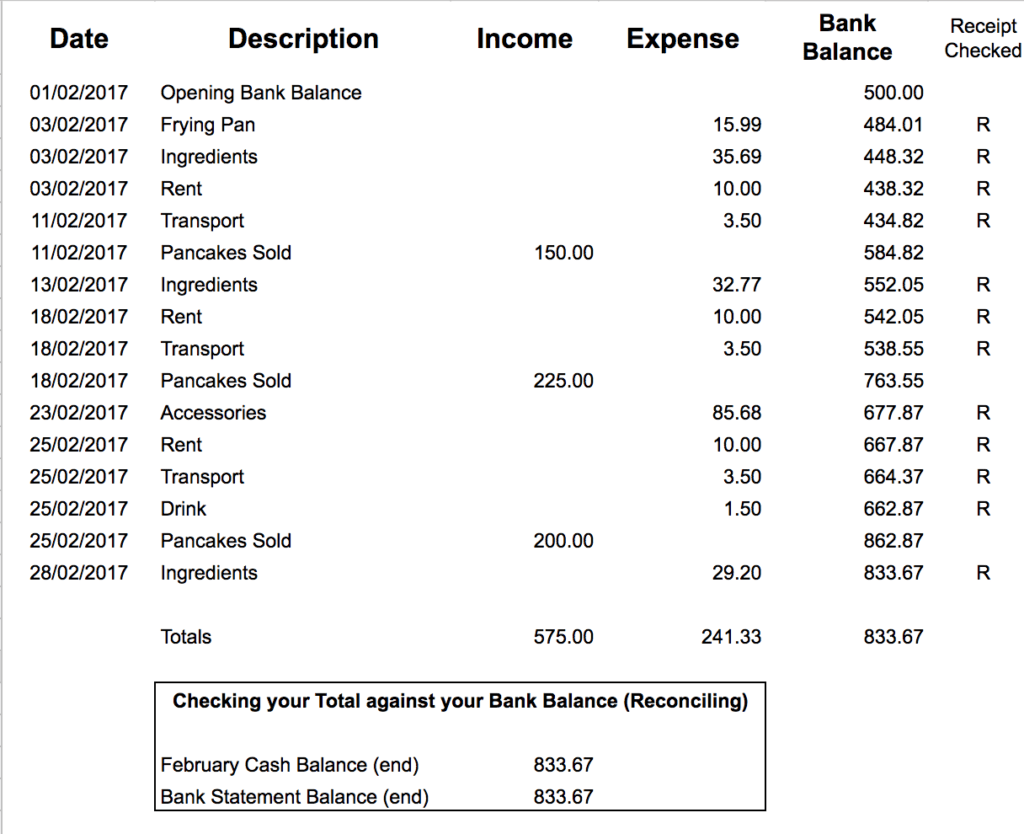

It looks like this in its simplest form:

But I would recommend making it a little more detailed so it can help you later on to benefit your business.

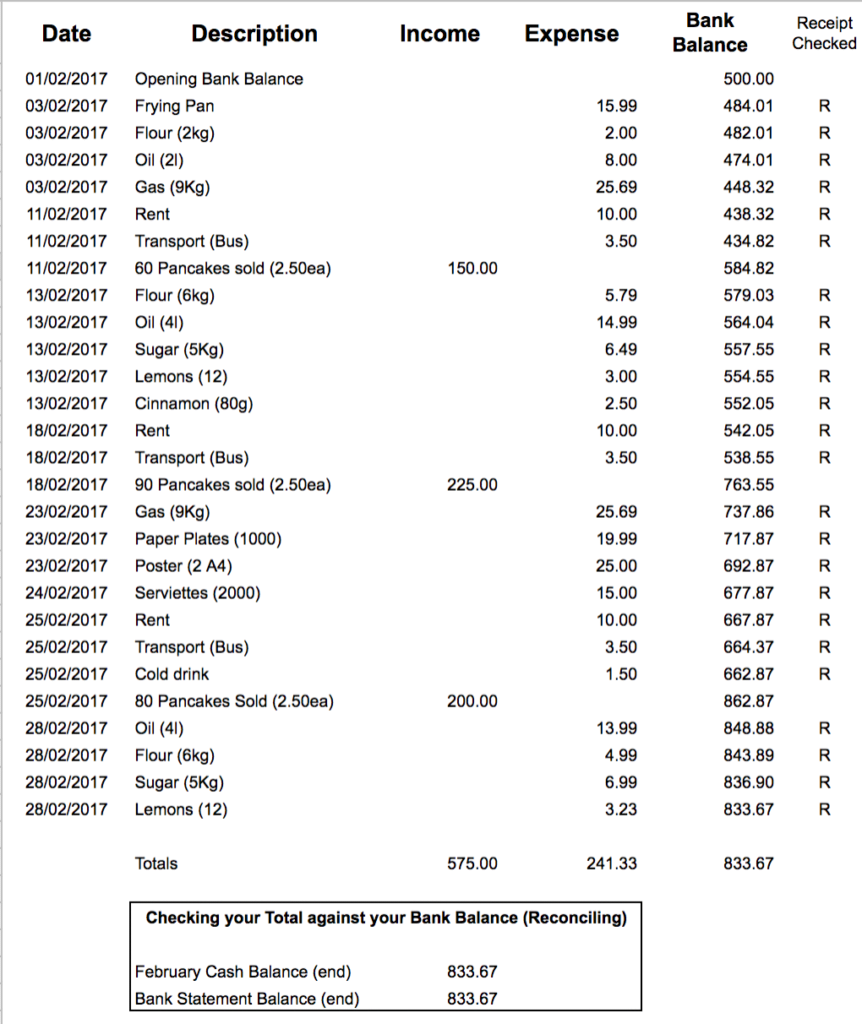

Here is a more detailed example:

You can copy this form by clicking Single Entry Accounting and editing yourself.

(Note: The R on the right side is where you match a receipt with your entry in your accounts and then filed it)

As you fill out each day you make sure you start with the previous day’s total, and you continue to add and subtract as you go.

At the end of the month, you check every item with your receipts, your bank statements and any invoices you have (outstanding or paid)

Then you close that months account with a total and a few notes.

It all begins again the next month and so it goes on.

You can do this in an A4 book or even in a special A4 ledger if you really want to be fancy!

Just make sure you get into the habit of keeping the record up to date. There is no point saying you will do it later and then wasting hours trying to ‘remember’ what that amount was you spent 27 days ago!

Wasted time means wasted money for you as an entrepreneur. Remember to make your time count!

Double Entry Accounting

This is the form of accounting which the majority of medium and large size businesses use. It is the best form of accounting in that if you cannot find something balancing in your records, you can find the problem by going back through your accounts and seeing where something was forgotten or mistyped.

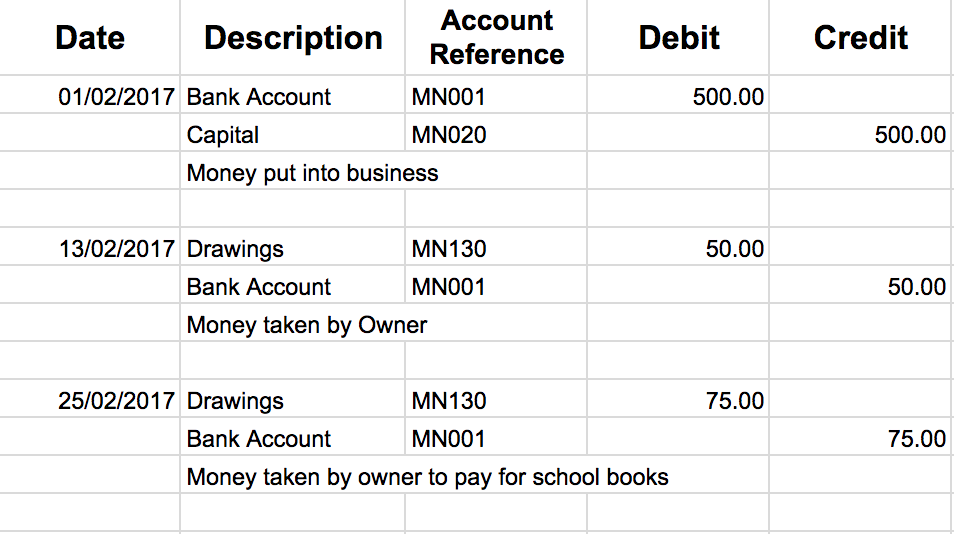

The way double entry accounting works is that you have one big ‘tin’ of capital and lots of little tins around it.

So you may have a tin called flour. In this form of accounting, you first need to make a note that you purchased flour, that means you need to show where the money came from.

You note that you take some money from the big tin and put it in the tin labelled flour. Then you make a note that you bought that flour for X amount in the small tin, and also note that purchase in the big tin. (double entry)

When you use that flour you then make another note that flour was taken from the flour tin.

Each time you make one note, you need to make another note somewhere else to show the money moving and changing into different things or back to money.

Each time it is a double entry.

These little tins are called journals and each product or service has its own journal. You will end up with lots of journals each month and each will show something coming in and something going out. It must balance.

If you ever wanted to know what accountants and bookkeepers do, that is it!

Here is an example of a journal:

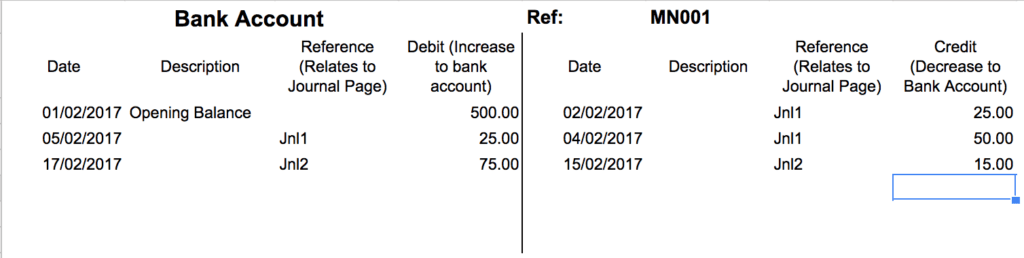

Each account reference is shown on a ledger and that shows the company accounts. Each entry must be detailed twice to show where it comes from and where it goes to. This must be shown in a General Ledger.

The reason for this is so that the journals show a running balance and importantly, track what is happening to your money and assets. The General Ledger will only give very brief detail with a reference pointing back to a particular journal.

Here is an example of a general Ledger showing the entries:

At the end of each month, the amounts are totalled and a final figure produced. This must balance with your main account and with your journal entries.

That information forms a Balance sheet which is produced to show how the business performed.

Today there are plenty of easy programs that will work this out for you and produce your accounts. If you go to Resources you’ll find I suggest Wave or Quickbooks. Both work very well to keep your accounts ordered and up to date.

When to Hire a Bookkeeper

You must keep good records and if you are able to maintain this together will all the other work you are doing then I will suggest you get used to it for the interim.

It will teach you so many lessons about how your business is run and make you very aware of how your money is being used.

If you are being overwhelmed by this process – STOP!

Stop trying to understand it, hire a bookkeeper and sit with them for a little while and establish what they need from you every week, month and year.

Then pay them the money to sort your books out for you. You will be better off asking someone to give you a quick break down of your account and financial situation than waste weekends and still not fully understand what is going on.

It will wear you down! You will be lifeless and drained by doing your books if it isn’t your thing and you cannot get your head around it just yet.

Rather consider that you will be a better creative person, salesperson or cook and will sell far more if you don’t need to worry about the financial side of things in their finer detail.

Make sure you account for the extra outlay for a book-keeper in your sales. Your first sale may be money that you spend on your book-keeper each day, so it will spur you on to make the next sale even more, to turn a profit from your business!

Conclusion

There are very complex ways of accounting, and there are simple ways. A simple one line for everything you buy or sell will work for a small business.

If you can grasp this and make it a little more detailed before moving onto grander things, I would suggest you try it. You will understand your money and business far better.

As I said though, if you are going to be overly stressed and you are going to lose even more sales and your creative flair, hire a bookkeeper and work with them to make your business better.

If you think this is going to be useful, let me know. Perhaps you are a wizard at accounts and want to let me know how we can all be better at it. (I know about the programs available, but lets first walk before we run!)

PLEASE NOTE:

I am neither a qualified accountant or financial advisor, so this is given purely for educational purposes. Anything you are unsure about I urge you to seek professional council over.

Get in touch with me through the Market Nosh Facebook Page or if you are a Trader offering advice to others or in fact asking for advice, why not visit the Facebook Group – Market Nosh Costers.

If you haven’t had a listen to The Market Nosh Show podcast, you can hear it by clicking Podcast above or visiting Soundcloud or iTunes directly to download it.

Quick Quiz

- Name two ways of Accounting

- What is Reconciling?

- When should you use a book-keeper?